A Note on Game Theoretic Approach to Detect Arbitrage Strategy: Application in the Foreign Exchange Market

Abstract:

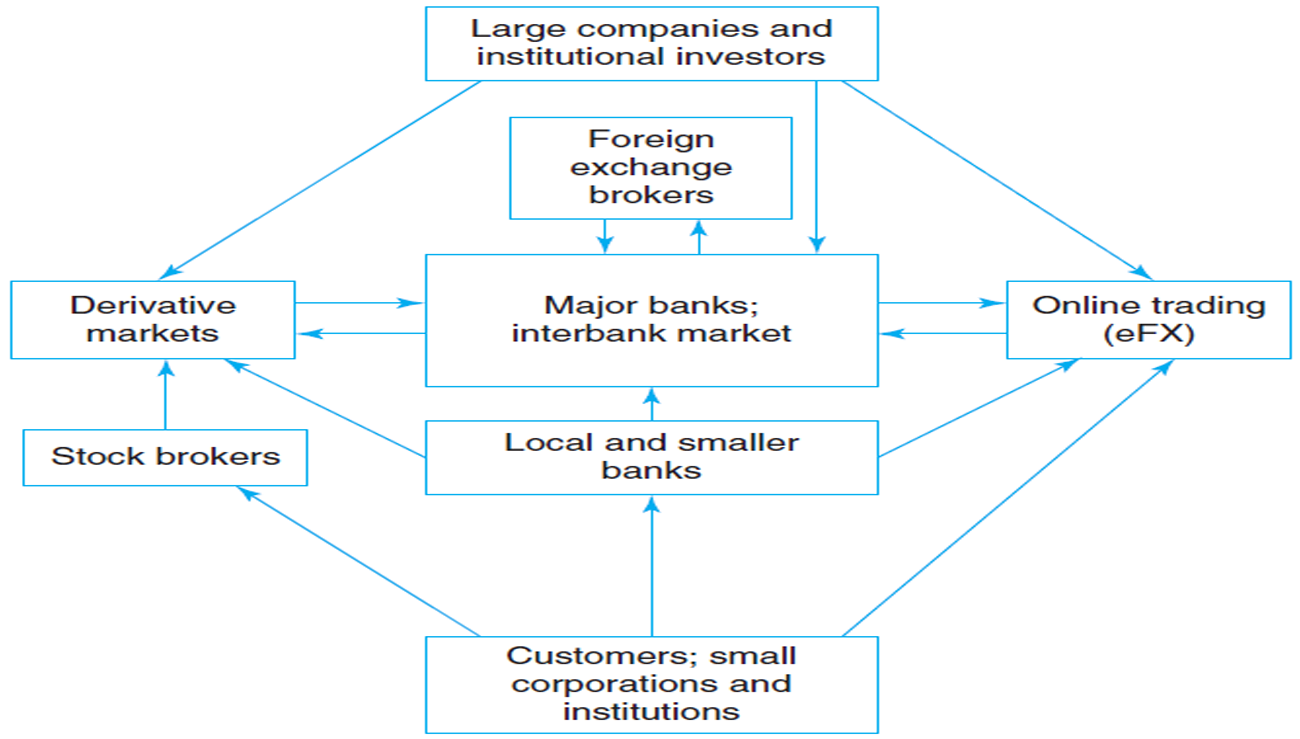

A game theoretic approach to detect arbitrage strategy in a foreign exchange market is proposed. Five propositions are given and then the optimal arbitrage path is derived.

Author(s):

Reza Habibi, Iran Banking Institute, Central Bank of Iran

DOI:

Keywords:

References:

Hao, Y. (2009). Foreign exchange rate arbitrage using the matrix method. Technical report. Chulalongkorn University. Bangkok.

Ma, M. (2008). Identifying foreign exchange arbitrage opportunities through matrix approach. Technical report. School of Management and Economics, Beijing Institute of Technology.

Raghavan, T. E. S. (1994). Zero-sum two-person games. In: Handbook of game theory with economic applications, Volume 2, Aumann RJ, Hart S (eds), Elsevier Science B.V., Amsterdam: 735–760. https://doi.org/10.1016/S1574-0005(05)80052-9